$1 Billion in 8 Months: Cognition Just Proved That AI Coding Agents Are Infrastructure, Not Features

The Devin round isn’t a bet on AI. It’s a bet on infrastructure that’s already working.

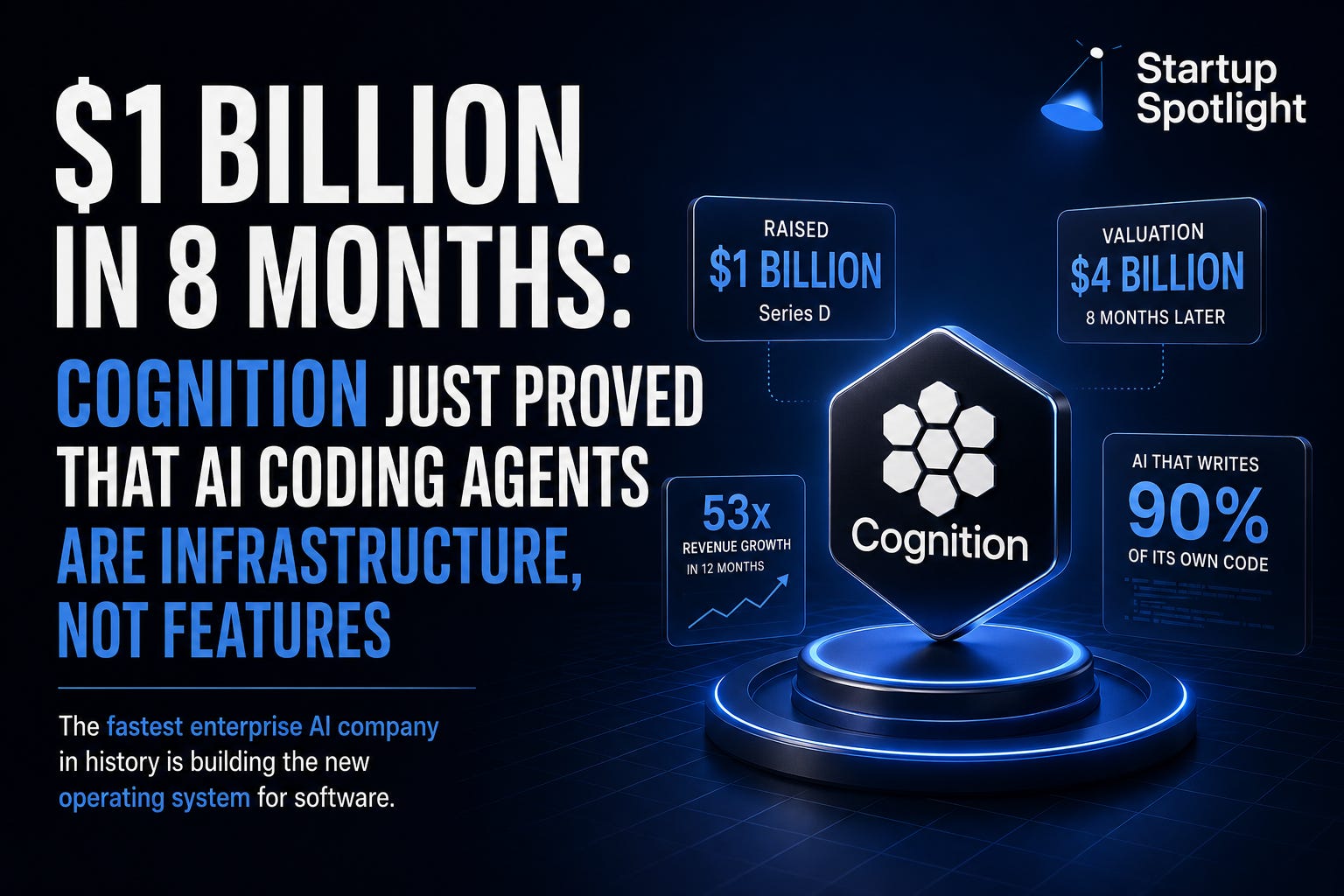

A two-year-old company that writes 89% of its own code with AI just raised $1 billion. That’s not a headline. That’s a signal.

Cognition AI closed a Series D at a $26 billion post-money valuation on May 27th, co-led by Lux Capital, General Catalyst, and 8VC, with Founders Fund, Ribbit Capital, and Atreides also in the round. The company has now raised over $2.5 billion in total since it was founded in November 2023. That’s three years of normal startup funding compressed into one.

The numbers behind it are even wilder. Cognition’s run-rate revenue was $37 million in May 2025. Today it’s $492 million. That’s a 13x increase in 12 months. They’re targeting $1 billion in annualized revenue before the end of 2026. Their enterprise usage grew more than 10x this year alone. Customers include Goldman Sachs, Mercedes-Benz, NASA, and multiple U.S. government agencies.

Their product is Devin, the AI agent designed to autonomously execute software engineering tasks. Not autocomplete. Not a copilot. Ownership. Devin took a legacy Mercedes-Benz system that would’ve taken a human team eight months to modernize and finished in eight days. That’s a 30x compression in time-to-delivery.

The competitive set matters here too. Cursor raised a $2.3 billion Series D in November 2025 at a $29.3 billion valuation and is reportedly in talks to raise again at $50 billion. GitHub Copilot, backed by Microsoft, is still the incumbent. But here’s the distinction that separates Cognition from both: Copilot and Cursor assist engineers. Devin replaces tasks. That’s a completely different value proposition.

Mental Model: Compounding Leverage

There’s a mental model I call Compounding Leverage in my book. The idea is simple. Leverage doesn’t add value linearly. It compounds. Every new capability you build on top of existing leverage doesn’t just make you a little better. It multiplies your output relative to your inputs across every future action.

Cognition is executing this playbook. Devin writing 89% of Cognition’s own code means their engineering team’s effective output scales without headcount. That savings compounds into faster product cycles, which compound into better enterprise contracts, which compound into more capital, which funds better models, which write more code. The flywheel feeds itself.

This is exactly what we think about at /mkt as we build inside a regulated framework. Every hour we don’t spend rebuilding compliance infrastructure from scratch is an hour compounded into product. Working with established infrastructure like tZERO for trading and operating under a Reg A+ structure means we’re not starting from zero on every problem. The leverage we inherit lets us move faster on the things that actually differentiate us.

Spence’s Take

Here’s the contrarian read: a $26 billion valuation for a company at $492 million in run-rate revenue is a ~53x revenue multiple. That’s a bet that the market for autonomous coding agents is so large, and so winner-take-most, that whoever wins it will justify that multiple on future numbers, not current ones.

That bet might be right. But it’s worth asking: at what point does the AI coding market look like every other platform war? Early movers set the standard, late movers get commoditized. Cognition is in a position where their own product can accelerate their own product development. That recursive advantage is real.

But if the models get cheap enough and commoditized enough, the moat shifts from the agent itself to the enterprise relationships, the data, and the trust. Goldman Sachs and NASA aren’t switching vendors every 18 months.

The builders who figure that out first won’t just have a good product. They’ll have a defensible business.