Apps Lost. Hardware Won. The Venture Capital Realignment You Missed.

Eclipse just proved that picks beat apps every single time.

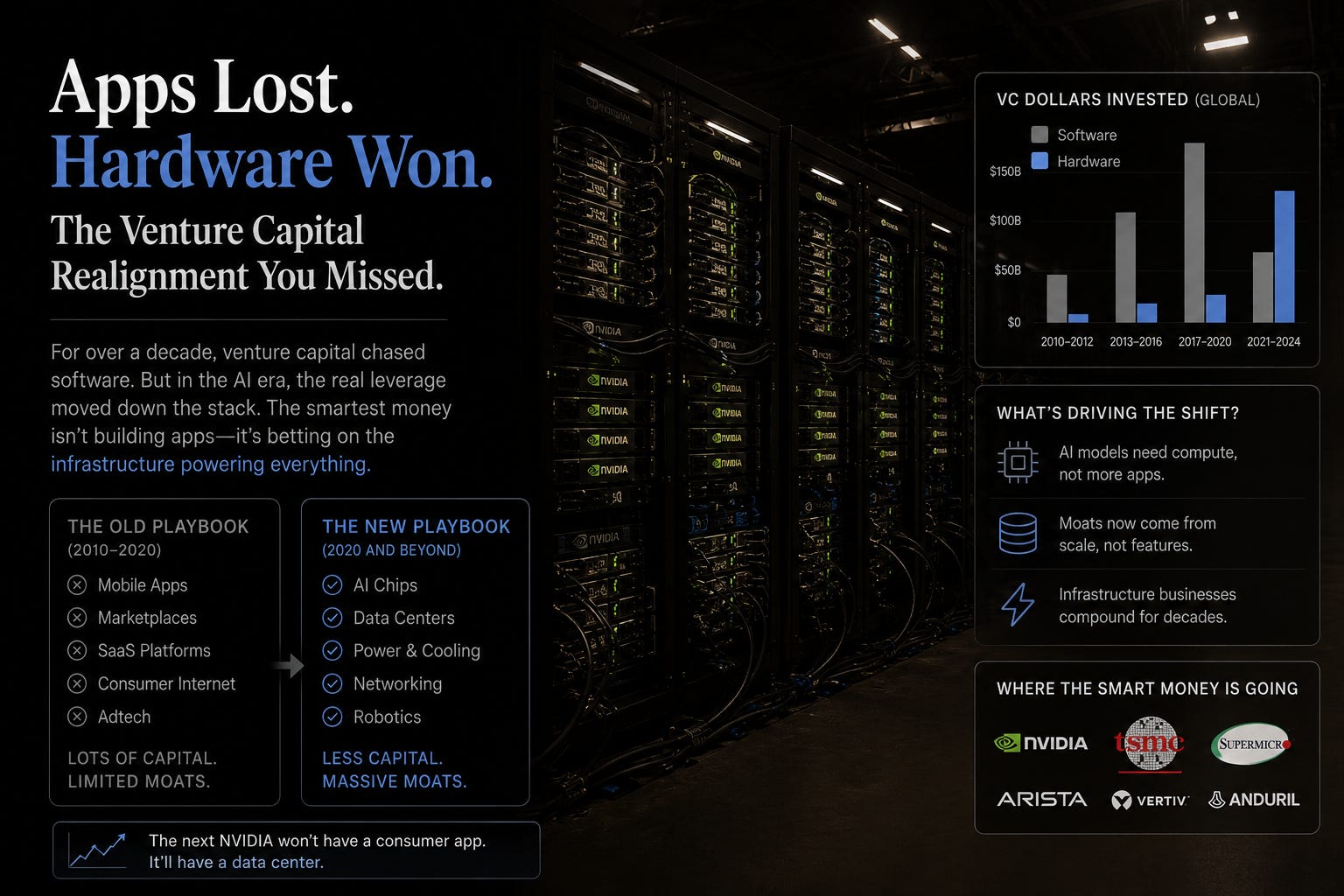

In 2024, VCs were investing in AI startups as if software margins mattered. They don’t anymore.

Eclipse Ventures just disclosed a $1.3 billion raise. $720 million for early-stage, $591 million for growth. Their focus? Not large language models. Not AI apps. Not SaaS wrappers around APIs. They’re backing physical industries: robotics, semiconductors, defense tech, manufacturing, and AI infrastructure.

Cerebras IPO’d two months ago. Market cap: $95 billion on day one. They make AI chips. Not software. Chips.

Figure just received orders for 70,000 humanoid robots. They’re production-constrained, not demand-constrained, and their revenue pipeline through 2029 is $14 billion+.

The pattern isn’t subtle. Capital is flowing from apps to atoms. From software to silicon. From SaaS to supply chains.

This isn’t a niche trend. In Q1 2026 alone, venture investors deployed $297 billion globally. Nearly half went into infrastructure, hardware, and manufacturing plays. The other half was split between frontier labs and everything else.

Here’s what happened: when AI made software cheap and easy to build, it destroyed software margins. Every idea can now be implemented in two weeks. That means competition is instant. Defensibility is near zero. Margin compression is real.

But you can’t build a frontier chip fab in two weeks. You can’t manufacture a humanoid robot in a sprint. You can’t scale power infrastructure with a prompt. That’s why capital is moving toward the things that are hard to build and hard to copy.

The mental model is Picking and Shoveling. When the California Gold Rush hit, the smart money didn’t pan for gold. They sold picks and shovels. Today’s picks and shovels are chips, robots, power systems, and the infrastructure that AI companies need to exist.

/mkt is a real-world test of this principle. We’re building in a regulated market (Reg A+) with infrastructure that’s difficult to replicate (tZERO for trading). We’re not trying to out-engineer a LLM. We’re building defensible infrastructure in a space where regulation is actually a moat, not a headwind.

Here’s the contrarian part that most founders won’t admit: if you’re building a pure-play AI software company right now, you’re already late. The capital has moved on. Your pitch will compete against a thousand other pitches. Your margins will be worse. Your funding will be harder.

But if you’re building infrastructure, manufacturing, or physical products that leverage AI as a tool (not your product), you’re swimming downstream with the capital.

The venture market is realigning. The question is whether you’re building the pan or the pick.

If this was useful, share it with someone who builds things. And if you want the full toolkit of 50 mental models, my book is coming soon.