ICEYE Went From €2.4B to €10B in Six Months. The War Isn't the Moat.

A €450M defense-tech round, a 4x markup, and the convex bet most people are mispricing.

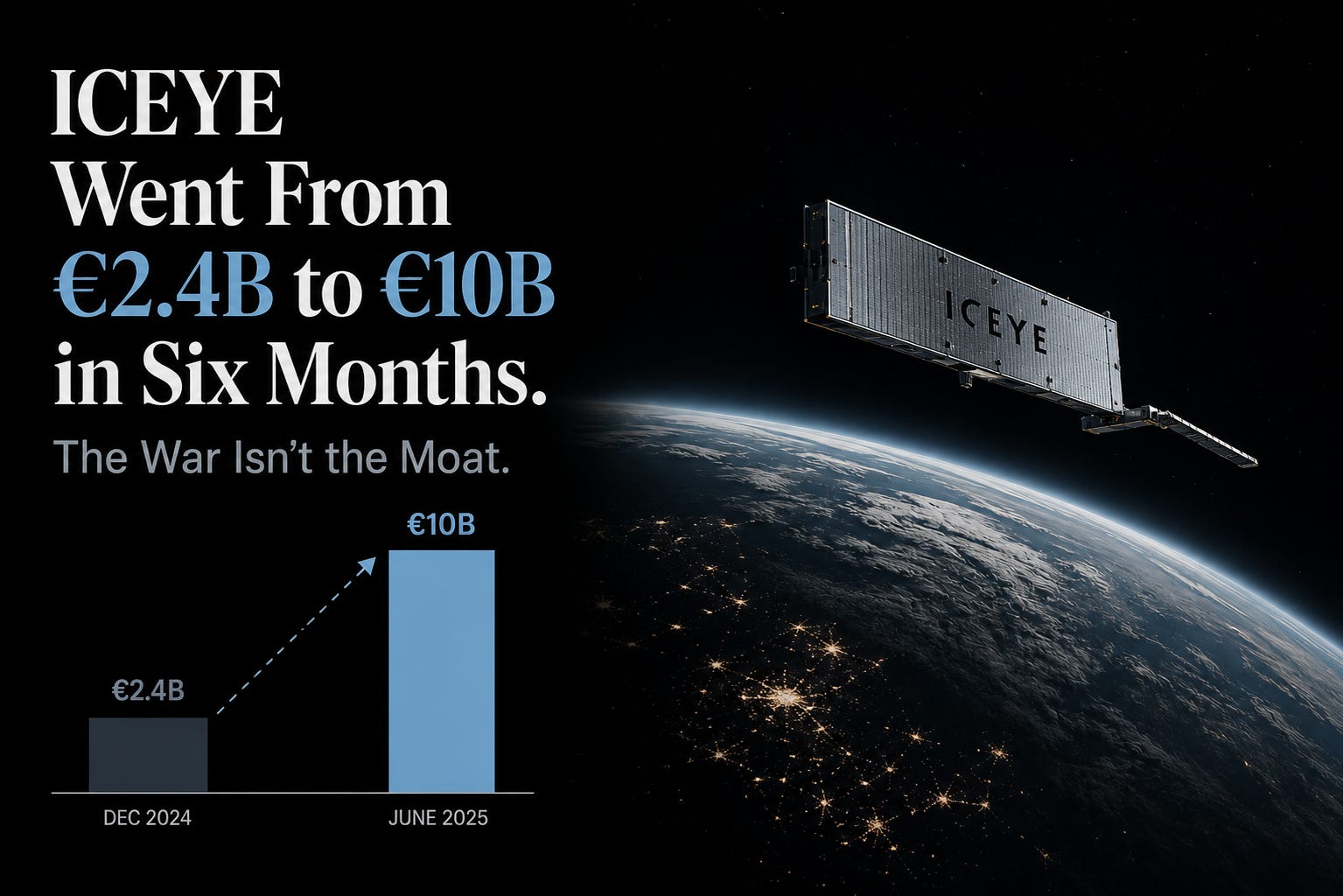

Six months ago, a Finnish satellite company was worth €2.4 billion. On Tuesday it raised at over €10 billion. That’s a 4x markup while the rest of us were doing holiday shopping.

ICEYE closed a €450 million ($520M) primary Series F led by General Atlantic at a valuation north of €10 billion ($11.5B). Add the secondary placement and the whole transaction clears €1 billion, one of the largest venture rounds ever for a European defense-tech company. New money came in from Nokia, the Qatar Investment Authority, TCV, and a stack of Finnish state-linked funds.

Here’s the part that matters: this wasn’t a slide deck. In 2025, ICEYE pulled in over €250 million in revenue, topped €100 million in EBITDA, and sat on a contracted backlog above €1.5 billion. Seven European governments have already bought sovereign satellite systems from them. They delivered Poland’s reconnaissance constellation in under twelve months and anchor a €1.7 billion German program with Rheinmetall. Seventy-two satellites up, the world’s largest synthetic-aperture-radar constellation, with production set to double to 100 a year by 2028.

The model: Convex Bets

A convex bet is one where your downside is small and capped, but your upside is large and open-ended. You pay a little, you can’t lose much, and once in a while you win big. The asymmetry does the work.

ICEYE’s entire architecture is a convex bet, and they placed it back in 2014. While legacy space programs spent billions on a handful of exquisite, slow-to-build satellites, ICEYE wagered on small, software-defined radar birds that are cheap to make and fast to launch. Each unit is a small, capped cost. Each one can anchor a national-security contract worth hundreds of millions (Poland, around €200M) or more than a billion (Germany, €1.7B). Capped downside per satellite, uncapped upside per customer. The €1.5 billion backlog is the floor. A continent that’s rearming is the open-ended top.

That’s not a hype premium. That’s convexity finally paying out.

My take

Everyone’s pricing the war. Ukraine, rearmament, “of course it’s up 4x.” But the war isn’t the moat, and wars end. The bet that actually matters is the cost structure: being the fast, cheap, software-defined option in a market where rivals still sell bespoke flagship programs.

And the convex upside only holds as long as governments would rather buy than build. So here’s the second-order question a 4x markup quietly skips: what happens when “sovereign” intelligence gets sovereign enough that nations want to own the factory, not rent the feed? That’s the bet under the bet. The backlog covers ICEYE for now. The next decade is the convex part, and it isn’t priced.

One more thing from where I sit. At /mkt we build inside one of the most regulated corners there is, and the ICEYE lesson travels. The friction everyone complains about (this deal itself needs regulatory approval before it closes in Q3) is the same friction that walls out the next ten competitors once you’ve cleared it. Hard to enter is hard to copy.

If this was useful, share it with someone who builds things. And if you want the full toolkit of 50 mental models, my book is coming soon.

This newsletter is for informational and educational purposes only. It isn’t investment advice, nor an offer or solicitation to buy or sell any security. References to companies, including /mkt, are illustrative and not recommendations. Figures cited are drawn from public disclosures and reporting. Do your own research and consult a licensed professional before making any financial decision.